Executive Summary

- During the month of April, the stock market experienced its biggest drawdown since markets began rebounding in late October 2023, as geopolitical tensions and higher inflation readings caused uncertainty.

- There are growing signs of a divergence in the economy, as higher income and wealthier consumers continue to spend above expectations while those at the lower end of the income and wage spectrum are being pressured by higher interest rates and higher inflation.

- We are now less than six months away from the Presidential and Congressional elections. As rhetoric and divisiveness ramp up, many are wondering how this could impact the economy and their investment portfolios.

- The committee also reviewed seasonality factors that tend to show lower returns and higher volatility from May to October.

- We want to remind our clients that patience is often the best course of action during times of uncertainty. However, we know that doing nothing, even when it is the right thing to do, is often emotionally difficult.

The members of the Investment Committee met on the afternoon of Tuesday, May 14th. Over the last month, markets dipped and then rebounded toward the all-time highs previously reached during the month of March. We were happy to have the opportunity to review and share perspectives from the economists and market strategists we follow.

After hitting an all-time high in late March, the S&P went through a fairly typical and seemingly orderly pullback of less than 10% during the month of April. This drawdown was primarily driven by two things. The first was a potential escalation of tensions in both Eastern Europe and especially in the Middle East when Iran directly attacked Israel for the first time ever instead of using its proxies in Yemen, Lebanon, and Syria. The second issue was the ongoing inflation pressures, as we received reports showing consumer prices coming in above expectations for the third month in a row.

However, over the last few weeks, the market has rebounded to within an eyelash of its all-time highs. This has been driven by corporate earnings for the first quarter coming in above expectations. Markets have also adjusted to the perception that the Fed will not be able to cut rates this year nearly as much as was expected as we turned the calendar into 2024.

The economy is also showing signs of a growing divergence between those at the higher end of the income and wealth spectrum versus those on the lower end. It appears that people near the top of these metrics continue to spend their income and wealth at levels above expectations despite higher inflation and higher interest rates. However, anecdotal evidence shows that these pressures are a strain on those at the lower end. This is showing up in credit card balances, auto and credit loan default rates, and the closures of a number of retailers that serve this segment of the population. This is something that the committee will continue to monitor and watch going forward.

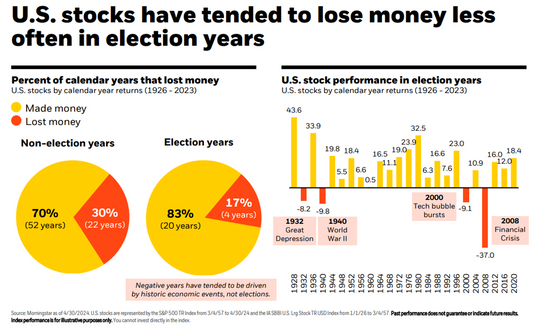

Committee members have also noted more questions and growing concerns from clients about the impact of the upcoming elections on the markets, the economy, and portfolios. As you can see in our first chart below, going back to 1926, the stock market has produced positive returns at a higher rate than its historical average during election years. As a matter of fact, the four negative years in the chart below were all driven by substantial economic or geopolitical events. The positive returns are partly due to incumbents trying to put into place policies that produce positive economic results in hopes of getting reelected. Please remember, this is true regardless of which party is in power. This is also driven by the fact that once election outcomes become more clear, it removes uncertainty, and this, in turn, tends to historically move markets higher.

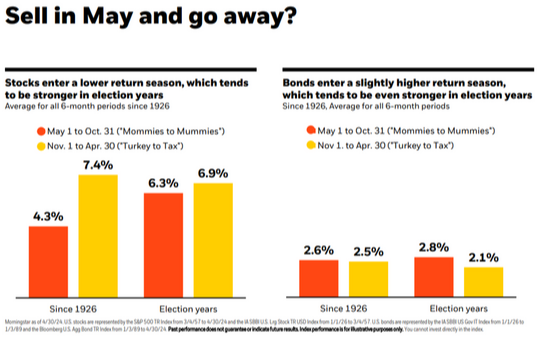

There is also an old Wall Street yarn that states that people should “sell in May and go away.” This thought process has been driven by the fact that stock markets have had stronger returns from November through April than they have experienced from May to October, as you can see on the left side of our next chart below. However, you can see that this phenomenon is less pronounced in election years. You can also see on the right side of the chart that returns in the bond market have been slightly stronger in election years during the May to October time frame.

We know that social media and the 24-hour cable news cycles will continue with negative headlines in order to get people to click or watch. Negative and alarming news sells and keeps people tuning in. However, it has historically not been in your best interest to adjust your investment portfolios based on the latest headline or crisis de jour. Warren Buffett has often said that “doing nothing when it is the right thing to do” is one of the hardest strategies for a successful investor to employ. Long time market strategist Jeff Saut has repeatedly stated that “patience is the rarest but most valuable commodity on Wall Street.”

Therefore, we would encourage you to allow your investment portfolio, which has been carefully constructed by your advisor to help you meet your and your family’s long-term financial goals, to do just that. We hope that as the weather turns warmer, you turn off the TV and back away from the computer and do what is most important in life, enjoy time with family and loved ones doing the things that make life meaningful to you. The committee and your advisor are watching things carefully and will take action if and when needed. In the meantime, if you should have any questions about your unique situation, please don't hesitate to reach out. We are here for you. Have a great day.

Investylitics Investment Committee

Jesse Hurst, Financial Advisor - Chair, Impel Wealth Management

Clint Gautreau, Financial Advisor - Horizon Financial Group

Nathan Ollish, Financial Advisor - Impel Wealth Management

Kevin Myers, Financial Advisor -ATL Global Advisors

Dusty Green, Financial Advisor - Spencer Financial Inc.

Grace Hayden MacNaught, Financial Advisor - Atlanta Planning Group

The views stated in this piece are not necessarily the opinion of Cetera Advisors LLC and should not be construed directly or indirectly as an offer to buy or sell any securities. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Past performance does not guarantee future results. Additional risks are associated with international investing, such as currency fluctuations, political and economic stability, and differences in accounting standards. Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. Additional risks are associated with international investing, such as currency fluctuations, political and economic stability, and differences in accounting standards.

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. A diversified portfolio does not assure a profit or protect against loss in a declining market.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe and is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.