Should you have any questions regarding these notes, please do not hesitate to contact Kevin at (678) 401-6102

At-A-Glance

7 min read

- In addition to the very real human suffering and atrocities we have witnessed in the war between Russia and Ukraine, we are also seeing a significant impact on the global economy, and more specifically the European economy.

- However, many economic reports, such as last week’s stronger than expected jobs report, continue to suggest that the United States economy is still growing and weathering the initial part of this storm better than most of the world.

- As we move into April, all eyes will be on the next inflation report, which is expected to be 9% or higher. The BIG question is whether inflation will peak soon and start moderating as we move further into the year.

- There will also be a close watch on first quarter corporate earnings reports. Many economists believe that earnings will outpace the relatively low expectations many companies have set. Guidance towards future revenues and profit margins will be extremely important to monitor.

- Volatility is real and expected to remain elevated throughout the year given the backdrop above, and the prospects of this year‘s mid-term elections. Diversification and regular rebalancing to take advantage of these swings is strongly recommended.

The Investment Committee met on the afternoon of April 4th to review our portfolio allocations and performance, as well as the economic and geopolitical backdrop we are facing today.

We are happy to report that the portfolios managed by the committee have held up reasonably well. They have performed in line with their risk adjusted, index-based benchmarks over the last one, three and five years. We are pleased with the relative performance of our models during this time of uncertainty.

We know that the internet and financial media are abuzz with negative headlines about the economy and the markets. Despite the news and noise, our portfolios are only slightly down on a year-to-date basis, and most of them still boast positive returns over the last year. We think it is important to keep things in perspective by looking at them over longer periods of time, rather than reacting to the daily headlines and market swings. Oftentimes, it psychologically pays to tune out too much news.

The war between Russia and Ukraine is significantly impacting the economy. From a global perspective it is putting supply constraints and adding pricing pressures to food, commodities, and energy prices. It is putting a further strain on the European economy due to the refugee crisis, the geographic proximity to the fighting, and Europe’s historically high level of reliance on Russian oil and gas. This is causing the outlook for European growth to be significantly reduced over the near term.

It may be surprising to many people that against this backdrop we are continuing to see strength in a number of US economic reports. A great example of this comes from the jobs report released on Friday, April 1st. The economy added 431,000 jobs last month. While this slightly missed expectations, there were positive revisions for the prior two months. And the unemployment rate fell to a new expansion low of 3.6%. This is just .1% less than where we were pre-Covid. As you know, jobs lead to income, and this leads to consumer spending, which makes up approximately 70% of the US economy. This bodes well for the US economy staying out of recession this year.

As we move into April, all eyes will be on the CPI report which is due to come out on April 12th. With the uptick in food and energy costs due to the war in Europe, already elevated inflation could take another bump higher. This could be complicated further by new rounds of Covid which are impacting China. This is causing shutdowns and supply chain constraints at Chinese port cities. It is important to remember that 6 of the 10 largest ports in the world are in China. We will be watching this closely going forward.

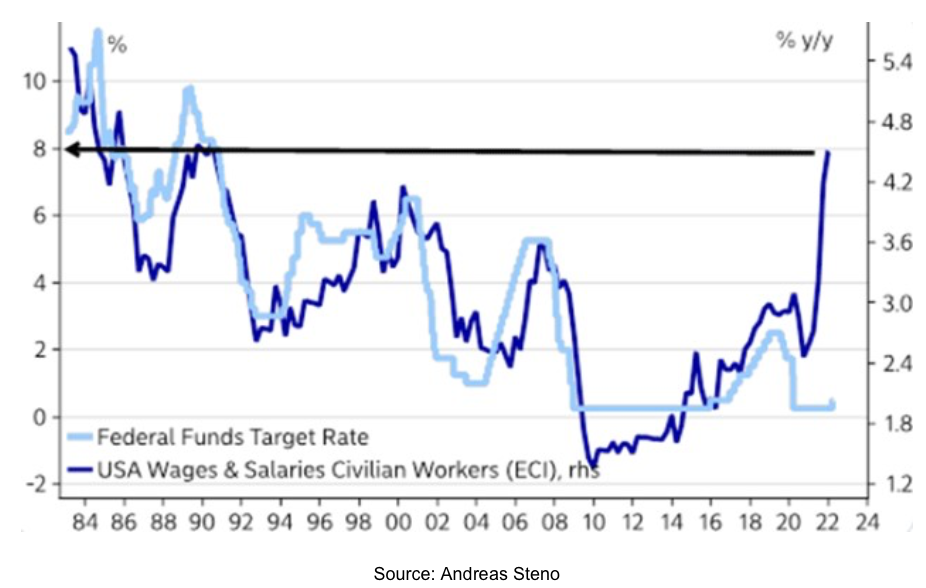

All of this will impact the Federal Reserve Bank’s future actions to combat persistent and rising inflation. After increasing interest rates for the first time in four years last month by 1/4 %, it is widely expected that the Fed could raise another 1/2 % at each of its next two meetings. As you can see from the chart below the Fed Funds rate has fallen significantly behind growth of wages and salaries, which it normally tracks closely. All of this will continue to drive mortgage and borrowing costs higher. At the same time, it could continue to put downward pressure on bond prices, which are already off to their worst start in more than 50 years.

Final Takeaway

We will also be turning our eyes towards first quarter earnings reports. So far, corporate America has been able to pass along higher wage and material cost to consumers in the form of higher prices. This has kept their profit margins intact so far. We will be closely watching the earnings releases and any future guidance towards revenue and profits.

Aside from avoiding the negativity of the news media during times like this, it is important to rely on sound portfolio construction principles. This means staying disciplined with your diversification and not responding emotionally to day-to-day headline news. It also means rebalancing from time to time to take advantage of market volatility. This allows you to sell certain asset classes when prices are up, in order to buy other asset classes that are down, over time, this has worked to the advantage of investors.

As always, the committee appreciates your trust in our process and portfolios. We work hard to manage the financial resources you entrust to us with wisdom and discipline. Please reach out to your advisor if you have other questions regarding your situation. Thanks, and have a great day.

Should you have any questions regarding these notes, please do not hesitate to contact Kevin at (678) 401-6102

Members of the Investment Committee

Jesse Hurst, Financial Advisor - Chair, Impel Wealth Management

Kevin Myers, Financial Advisor - 30A Wealth Management

Clint Gautreau, Financial Advisor - Horizon Financial Group

Nathan Ollish, Financial Advisor - Impel Wealth Management

Joy Schlie, Financial Advisor - FHT Financial Advisors

The views stated are not necessarily the opinion of Cetera Advisors LLC and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing.